The State of Early-Stage Fundraising in 2026

It has never been a more thrilling time to be building and investing. With over $300 billion deployed, the first three months of 2026 marked a historic quarter for venture capital.

Global Venture Dollar Volume by Stage, by Quarter (Q1 2023 – Q1 2026)

At the same time, it can feel bewildering and overwhelming. In North America, nearly two-thirds of all investment capital was concentrated in a handful of companies: OpenAI, Anthropic, xAI, and Waymo. Alongside them is a growing list of AI research and infrastructure startups — the “Neolabs” — many of which are already valued at over $1 billion, despite generating little or no revenue.

While the total deployed capital has skyrocketed, the volume of deals is actually declining. Q1 2026 saw under 4,000 deals, down from over 5,000 in the same period last year.

Global Seed and Angel Investment by Quarter (Q1 2025– Q1 2026)

Artificial intelligence has created one of the most dynamic fundraising environments the venture industry has seen in decades. It has also introduced real uncertainty: concerns around disruption to existing industries and SaaS categories, and hard questions about defensibility. And what about the companies that are not “AI-native?”

Drawing on publicly available and internal data, and our own experiences leading and supporting financings across the Reach portfolio, this report explores what’s driving early-stage deal sizes and valuations, how expectations are changing around growth and storytelling, and other dynamics that shape these rounds. Building on these insights, we also offer practical tips to help founders better prepare for future fundraises.

Explore the full report below, along with commentary from a recent presentation we gave to our portfolio. Buckle up!

What’s Driving the Tale of Two Venture Markets?

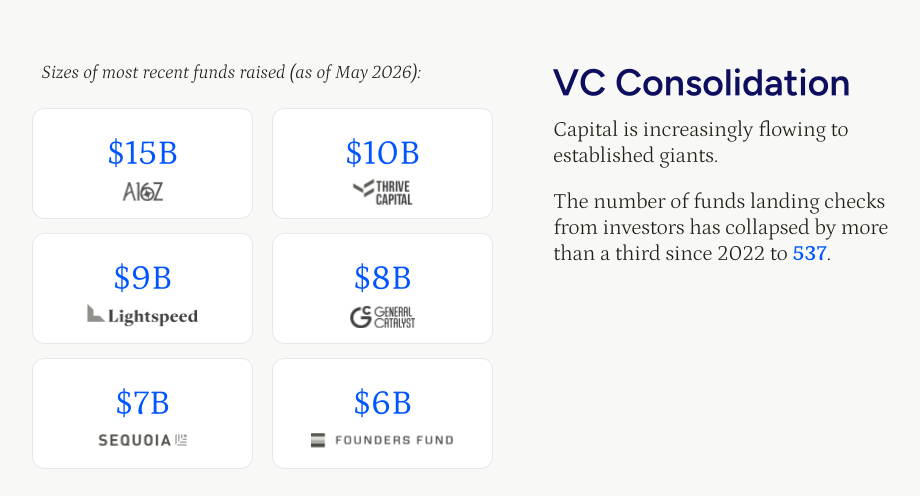

Just as venture capital funding has concentrated around a handful of mega AI companies, institutional capital has similarly consolidated among an increasingly small group of mega-funds raising ever-larger vehicles.

On the other hand, the total number of venture capital funds has dropped dramatically by more than a third since 2022, from 1,609 to 537.

The ability to raise new funds is, of course, dependent on performance. So far, the post-pandemic exit environment has been sluggish. The handful of IPOs that have made it to market have largely underperformed, and we await hotly anticipated mega-offerings from SpaceX, OpenAI, and Anthropic.

To date, many venture funds have yet to deliver meaningful returns to their limited partners. With continued pressure on DPI (a key measure of how much money they have returned to investors), many firms have become more aggressive but also more selective in backing their highest-conviction companies.

What Does This Mean for Founders?

Capital exists, but it is concentrated. Record dry powder and a record quarter are evidence investors are deploying and that rounds are still getting done. We recommend founders run a two-tier strategy, targeting top-tier generalist investors and category specialists in response to the increasing stratification of the VC landscape.

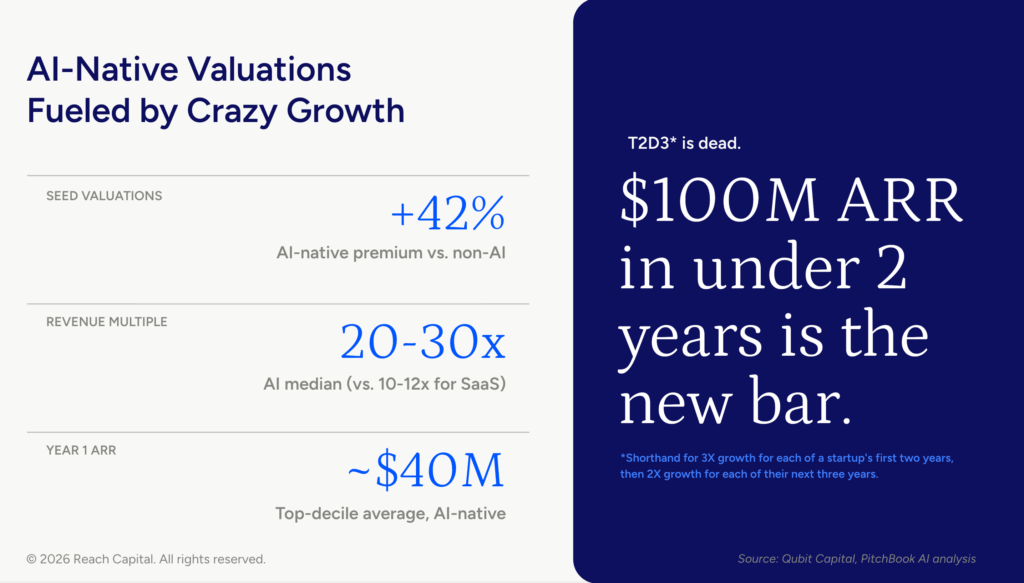

The AI premium is real. The data shows there is a 42% premium on seed rounds for AI-native companies. We are seeing 20X to 30X revenue multiples for many of these rounds — and in some cases upwards of 50X — compared to the 10X we previously saw a few years back for SaaS companies. Startups that reach $100 million in under two years have raised expectations for everyone, and top AI performers report an average of $40 million in ARR in their first year.

For fundraising narratives today, AI-native positioning commands attention. Companies that are not must work to differentiate themselves and establish defensibility. This does not mean, however, that founders should just slap AI on businesses where it is not authentic.

We have seen founders successfully raise a clear and compelling narrative about how their businesses are AI-proof. During her Series A process, Jen Wirt, CEO and Founder of Coral Care — a marketplace for at-home pediatric services — articulated a strong narrative around how human care cannot be replaced by AI, even as many of its growth, margins, and operations have been greatly improved by it. (She closed a $13M Series A earlier this year.)

There will inevitably be funds that are only focused on AI-native solutions with little or no humans in the loop. If that’s not your company, don’t waste your time trying to convince them otherwise.

Exit paths matter: Feeling pressure to return capital to LPs, many investors have exit outcomes and liquidity timelines in the back of their minds.

At the same time, founders — particularly at the early stage — should refrain talking about exits too directly. Instead, frame the conversation around market size, the potential for expansion, and the catalysts that could drive growth. (In education, for instance, we are following the growth of ESA programs.) Talk about inflection points, shifts in customer and buying behavior, adjacent markets, and why your company is uniquely positioned to capture these opportunities.

In other words, without saying “exit” explicitly, make it easy for investors to connect the dots between the size of your market (the “TAM”) and the size of their potential returns.

Sector and Reach Portfolio Benchmarks

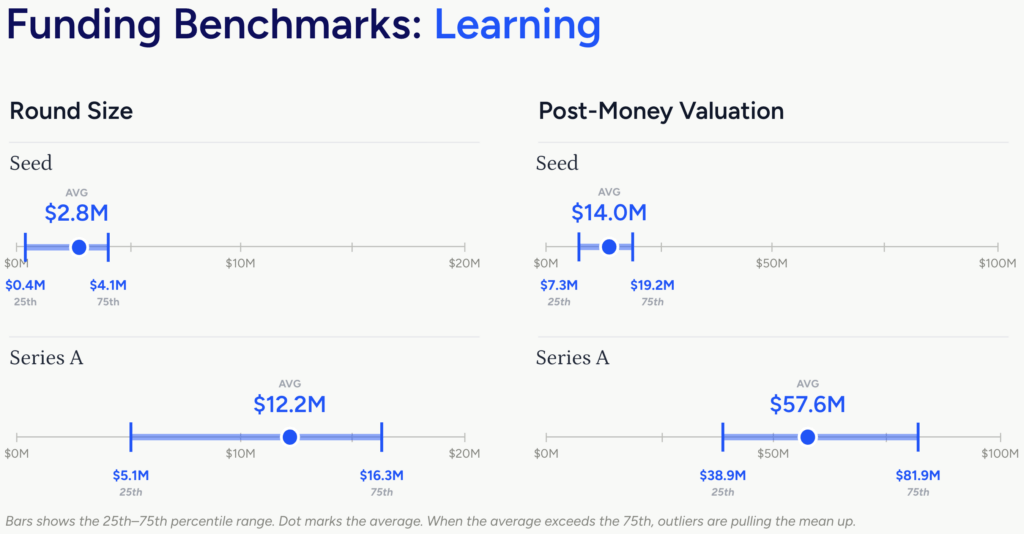

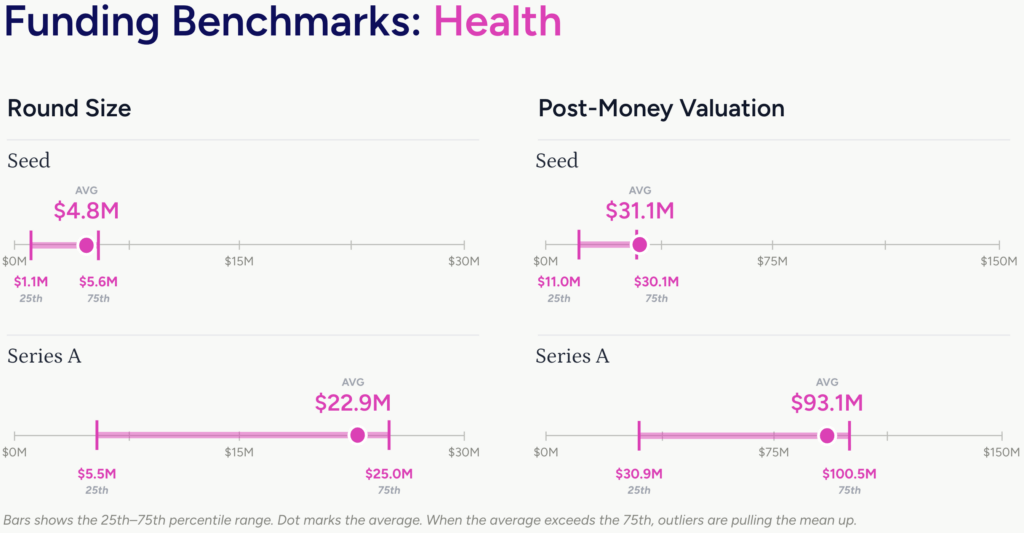

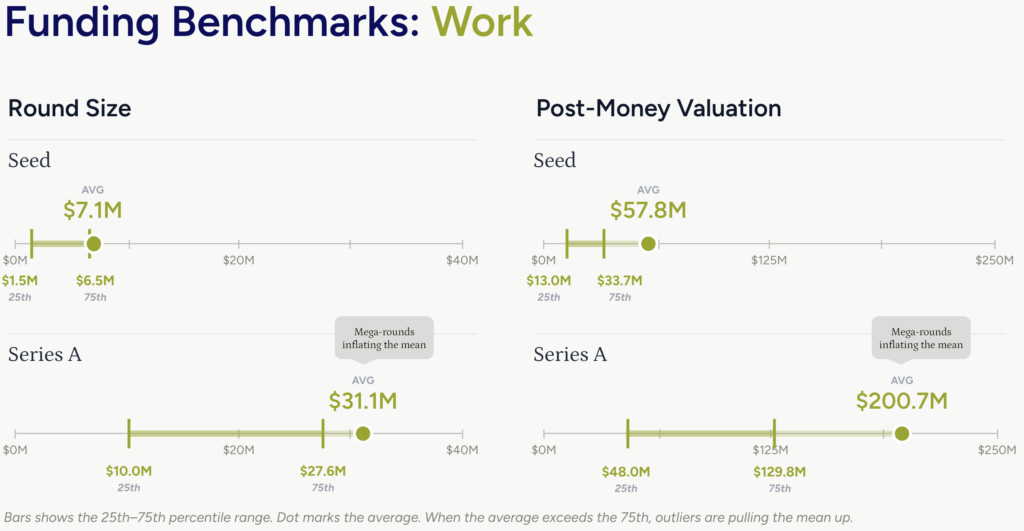

The charts below, created using both public and internal Reach data, show the range of round sizes and post-money valuations for Seed and Series A deals in learning, health, and work.

The colored line shows the 25th to the 75th percentile range, and the dot is the mean average. When the dot is closer to or above the 75th percentile, it means there are mega rounds that pull up the entire industry averages.

Learning: In learning, the mean average round size has stayed within the middle of the valuation band, reflecting the fact that there have been fewer outlier rounds. Relative to other industries, learning and edtech continue to face a more challenging raising environment. Still, there are standout examples of AI-native learning tools raising at attractive multiples from top-tier generalist investors, such as Outsmart and Oboe.

Recent data from Carta places edtech in the lower band in terms of round sizes and valuations. We believe the full picture is more nuanced, particularly as learning intersects with adjacent sectors like health and work (such as Stepful from our own portfolio). To the extent that an edtech company overlaps with other sectors, it can be advantageous to highlight those adjacencies during fundraising.

Health: Health tech most closely mirrors the broader overall venture funding market. Since 2025, there have been about a dozen mega deals driving up these average round sizes and valuations, for companies like Slingshot AI ($93M Series A), OpenEvidence ($75M Series A), and Tala Health ($100M Seed).

Across any of these deals, AI has become table stakes in the company narrative. Those that have credible data moats or are focused on consumer products and services are commanding the highest prices.

Work: This category is where mega rounds are inflating the mean averages the most, particularly at the Series A, even though the realistic post-money valuation falls more closely in the $50 million to $130 million range. Many of the deals getting funded in this space are embedding agentic workflows in specific verticals, such as Corgi for insurance, and can demonstrate measurable results: clear dollar savings, hours reclaimed, outcomes improved for end users.

Reach Portfolio Takeaways

This scatter plot below shows data from select Reach portfolio financings over the past 12 months.

Select Seed and Series A Rounds (May 2025 – May 2026)

Some takeaways:

The highest-valued companies power the AI economy. The outliers tend to operate in categories tied to data infrastructure and workflow automation.

Bridges are a new norm. The cluster of smaller round sizes at still-healthy post-money valuations signals founders are increasingly willing to accept some dilution in exchange for capital to reach the next milestone. According to Carta, about 29% of all deals at both the seed stage and Series A were bridge fundings in 2025.

Bridge rounds sometimes carry a negative signal. But that’s not always the case, particularly in an environment where capital is abundant. Many bridges today are being raised opportunistically by founders who are not quite ready for a Series A or B process and need some extra runway to reach those milestones (more in next section).

Round sizes and post-money valuations are loosely correlated, which suggests there is no rigid formula of how financing terms come together. These figures are sometimes set more on the strength of the founder and team than market benchmarks. That said, there is still meaningful concentration around the $50- to $75 million post-money valuation range, which is a good benchmark for a Series A round.

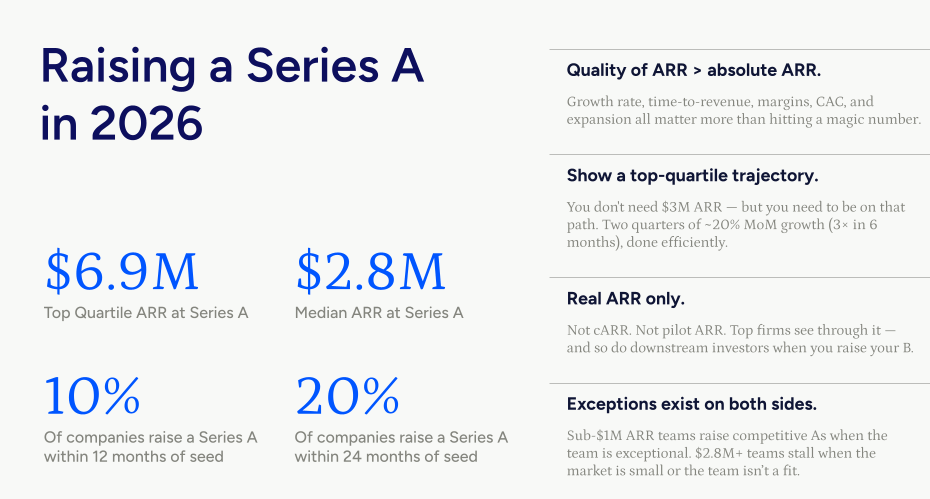

Raising a Series A

What does it take to raise a Series A in today’s environment?

According to Carta, top-quartile Series A companies are generating nearly $7 million in ARR, although the median is closer to $3 million. Of companies that raise a Seed round, 10% of them close a Series A within the next 12 months, and 20% within the next 24.

The bar has certainly risen. While these figures can seem intimidating, there are some nuances to take into account:

The quality of the revenue is more important than the absolute number itself, and good investors will recognize that. Growth rate, time to revenue, margins, retention, expansion, efficiency — all of these things matter more than one magic number that may look weak when under scrutiny.

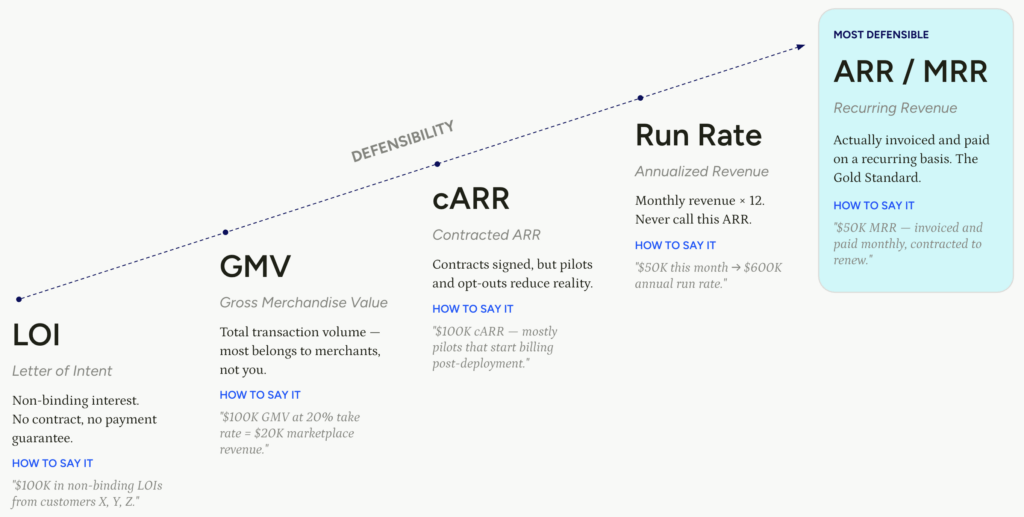

Real revenue is what founders should be pitching. Today, we’re seeing creative (and sometimes misleading) figures being presented as real ARR, including pilot revenue, contracted revenue, and other forward-looking projections. Good investors will know the distinctions, so it’s important to show what’s real.

Below is the spectrum of different revenue types, from most aspirational (and least compelling) to the most durable and defensible, adapted from Garry Tan’s helpful framework.

Show a top-quartile growth trajectory. Very few companies are actually at $7 million in revenue when they raise a Series A. You do not necessarily need to be there. But do show a compelling growth trajectory for how you get there efficiently.

Every raise is an exception in some way. There are exceptional founders with under $1 million in ARR who still close competitive Series A rounds because the team, product, or market is exceptional. (We have done several multiple pre-monetization Series As ourselves). At the same time, there are teams with over $3 million in revenue but struggle to raise because growth is stalling or the market is facing headwinds. In other words: Don’t get too affixed (and intimidated) by benchmarks.

How to Run the Right Process: Pro Tips

A good fundraising process can make a company. A bad one can end it.

Before reaching out to investors or putting a data room together, pull some comps. Look at companies in your space or an adjacent one, their round size, and what valuation they raised at. Ask founder friends to share which investors were in the mix, who led, who followed on, who balked, and how they presented their story. Ask about where their company was from a revenue and traction standpoint.

The two most common paths we see: raising a bridge (or extension) round, or a full Series A from a position of strength.

An extension can make sense when there’s a clear line of sight toward top-tier metrics, but the company needs a little more time. For these rounds, discipline matters. Avoid running an overly broad process with dozens of meetings, and timebound it. Speak to your existing investors first, followed by a handful of strategics. Operator funds can be great here, but try to keep it to 10 or less targets.

A full Series A, by contrast, can be an extensive, time-consuming process. We recommend pursuing this when you have cleared the bar on metrics and have an extremely compelling story to tell about how much faster and bigger you can grow.

As you prepare for the fundraising journey, here are some pro tips we consistently share with founders:

- Partner targeting, not firm targeting. Every partner has distinct tastes, interests, and convictions. Focus on finding the individual within the firm who is aligned with your space or business model.

- Do practice runs. Take 2-3 meetings with non-target firms first to refine the pitch and stress-test objections. Then hit your target list when you’re sharp.

- The reference call ambush. Investors will backchannel and call your customers, ex-employees, and employers. Pre-brief them. Encourage your strongest supporters to reach out proactively.

- Diligence room readiness. Have a clean data room ready before you open meetings: financial model, cohort data, customer references, cap table, key contracts, org chart.

- Detect “no’s.” VCs rarely say no outright. They usually say “let’s stay in touch.” Learn to read these signals. Put them on a quarterly update list.

- Don’t stop building. Close a customer, ship a feature, hit a milestone during the raise. Every meeting where you can say “since we last spoke, we just did X” rebuilds momentum.

- Raise when your momentum is strongest. Consider what is cyclical about your business and raise at the height of the cycle.

- Manage your existing investors actively. Your current investors are your biggest asset. They can signal support and make helpful introductions.

- Take care of your mental health! You’ll get 100+ no’s. Each one feels personal. Get support from founder friends who have faced this.

If you’re thinking about your next raise or have questions, please reach out! caoimhe@reachcapital.com

Read the full 2026 State of Early-Stage Fundraising report.

Read the Latest

News and Insights