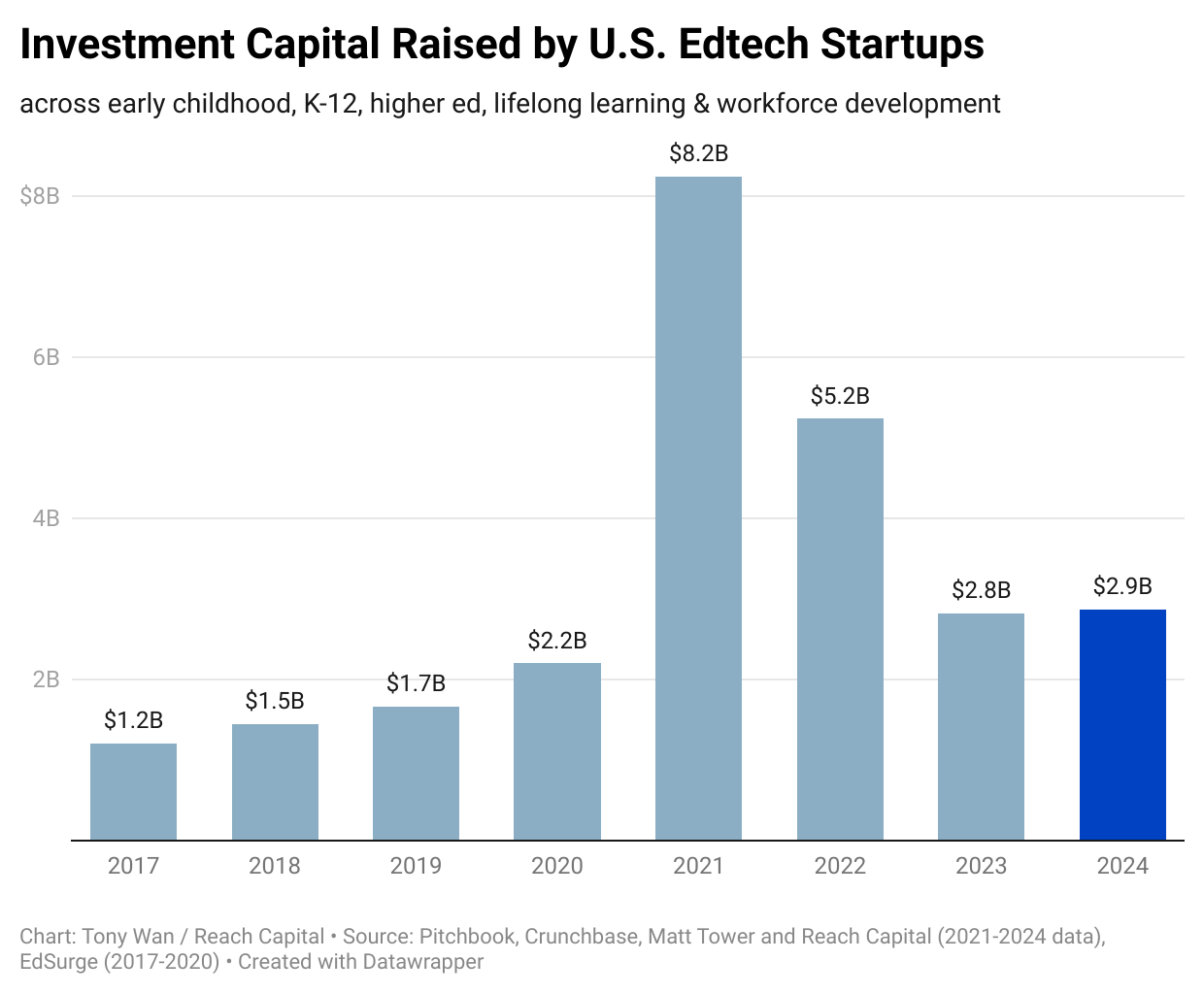

At $2.8B, 2023 U.S. Edtech Funding Is Back… to Pre-Pandemic Days. But in a Very Different World.

Last month Zum announced it had raised $140 million at a $1.3 billion valuation. The school transportation startup is not your typical “edtech” startup; most don’t own and operate a bus fleet. Still it’s a rare sighting: such figures and marquee growth investors — in this case Sequoia Capital and Softbank — have been largely absent in education deals for over a year.

So is edtech back? Yes — but not in the way one may think.

Looking at the 2023 totals for U.S. edtech investments, edtech indeed is back… closer to pre-pandemic levels, before the market was awash in relief funds and buoyed by record-low interest rates. With traditional growth-stage rounds and investors largely absent from edtech for the last 18 months, investments in U.S. edtech companies totaled $2.8 billion in 2023. (Setting aside the biggest investment — Cengage’s $500 million raise from Apollo Global to pay back its debt — that tally dips to $2.3 billion, which is on par with 2020 levels.)

This analysis is based on our review of 218 deals surfaced through Pitchbook, Crunchbase, ETCH and internal data. We define “edtech” as companies that primarily focus on teaching, learning and increasing access to economic opportunity, across early childhood, K-12, higher ed, workforce development and lifelong learning. The last category refers to personal development not explicitly tied to academics or work, such as language learning.

Falling investment totals mirror broader macroeconomic headwinds and are certainly not unique to the edtech sector. Healthcare, a sector with market dynamics and characteristics similar to education, saw funding retreat to 2019 levels. According to Pitchbook, overall 2023 global venture funding fell back to 2019 and 2020 totals.

Starting in the second half of 2022, rising inflation, interest rates, geopolitical crises and belt-tightening brought an end to the copious amounts of capital that defined the pandemic. Many companies that raised at the peak have struggled to grow into rich valuations.

Attributing to the dramatic dropoff for U.S. edtech in 2023 was the disappearance of mega rounds exceeding $100 million. In 2021, 21 deals exceeded this threshold. Last year, there was just one: Amplify’s $350 million Series C round from Cox Enterprises, Learn Capital, A Street and Emerson Collective.

What’s also missing on this year’s billboard chart: consumer education plays, with the exception of HOMER. The return to classrooms and offices, and likely some newfound appreciation for in-person social experiences after isolating during the pandemic, are plausible factors. Inflation is another. Consumers (finally) slowed their personal spending toward the end of last year, and investments in direct-to-consumer retail and e-commerce took a big hit.

Notably, most of the businesses on this list sell at the enterprise level: providing K-12 districts with digital curriculum (Amplify) and substitute teachers (Swing), supporting higher-ed academic operations (Coursedog) and student mental health (Uwill), and helping other companies train staff (Transfr, Sana Labs, Degreed). These systems continue to seek solutions to help people adjust to post-pandemic challenges around staffing, well-being, and reskilling in the age of AI.

Aside from mega rounds, there were also notably fewer later-stage venture rounds — Series B, C and beyond. Compared to 2021 and 2022, deal volume at these stages fell by roughly half in 2023. Many deals were done as extension and bridge rounds to help companies extend their runway.

Indeed, the investing numbers are sobering. But on the exit side there are better signals. As industry analyst Matt Tower has noted, the majority of publicly traded edtech companies beat the S&P 500 last year. And there have been some sizable exits: Goldman Sachs’s $1.72 billion purchase of Kahoot; Instructure’s $835 million acquisition of Parchment; PowerSchool’s $300 million acquisition of SchoolMessenger. Later this year, early childhood management software Procare will be acquired for $1.75 billion. Private investors take cues from exits and public markets, and prospects for IPOs in the broader tech sector are starting to revive.

And while the number of seed rounds declined from 2022, activity at the angel and pre-seed levels remain robust. With AI lowering the cost and time needed to build and launch into the market (particularly native Generative AI tools), there has been a flurry of pre-seed deals for those that have shown early traction.

A host of new edtech venture studios and accelerators have also emerged to provide guidance to early-stage founders (carrying the torch first lit by Imagine K12, which incubated many big education brands including ClassDojo and Clever). And as our peers have expressed, the quality of early-stage startups is higher than ever. We agree.

The AI Bump

Bucking the funding downturn, of course, were the mega AI rounds. Led by OpenAI, Anthropic, StabilityAI and others building foundational models, AI startups raised nearly $50 billion in 2023.

Edtech has yet to command such outsized deals, but they may not be far away. Replit, which has been building AI assistant tools for developers, raised $97 million in its Series B extension. Education apps were among the earliest demos showcased by OpenAI, which is continuing to expand its footprint with recent partnerships with Arizona State University and Common Sense Media.

“Copilots” for classroom teachers, along with language-learning tutors, course-authoring platforms and autograders are among the most popular AI tools we’ve seen in our pipeline. For seed rounds these companies did command higher funding totals and valuations than the overall average deal, but not by an extravagant amount. For Series A valuations, though, AI companies command a premium.

Demography Is Destiny

Artificial intelligence may be the future. Closer to the present, school systems are strained by very real human challenges, the magnitude of which are reflected in the deals we saw — and backed — in 2023.

K-12

Student enrollment remains below pre-pandemic levels and chronic absenteeism is growing; more than 14 million kids missed more than 10 percent of school days. Teacher and counselor shortages, turnovers and the declining graduates from teacher-prep programs are bubbling up to an “epic crisis.” Simply put: strapped for staff, schools need help.

Many K-12 edtech deals concentrated around efforts to build human capital and expand the capacity of schools to serve the growing needs of students. Swing ($38 million Series C) connects school districts with subs; Coursemojo ($4 million Series A) beams remote teachers virtually into classrooms. Cartwheel ($20 million Series A) and Clayful ($7 million Seed) connect schools with coaches and professionals to provide mental health support.

We’ve also seen more tools focused on serving neurodivergent populations — services like Marker and Sharpen that diagnose and support students with ADHD, dyslexia and other learning and attention disorders. Federal and state funding contribute to a $80 billion market for special education services, but accessing these require diagnoses and interventions that for too long have been costly and timely.

Related to human capital movements are two financial capital trends we’re monitoring closely:

The growth of ESAs. Thirteen states now offer some form of education savings accounts (ESAs) that redirect public dollars to parents to spend on educational services of their choice. Homeschooling is on the rise and alternative options are proliferating: new school models like Sora; online classes offered on Outschool; and microschool incubators like KaiPod that help educators start and operate their own schools. These new models also attract teachers who desire more flexible schedules and sustainable work. Over the last few years, over $1.5 billion ESA dollars have gone to families, and this number will continue to grow.

The end of ESSER. The fateful day is drawing near. ESSER III (the last tranche of the $190 billion in federal pandemic funds for K-12 education) must be committed by the end of September. School leaders we’ve talked to are already preparing the chopping block for tools and services that are nice to have but not a necessity, and those that fail to show usage and efficacy. Every K-12 entrepreneur should pay heed.

Higher Education

In 2023, undergraduate enrollment finally returned to growth for the first time since the pandemic. Still, public sentiment on the ROI of higher education continues to sour; more than half of parents now don’t want to send their children to a four-year college. There is much more value to college than just landing a job, but unrelenting tuition increases force financial considerations to the forefront.

Notably, the biggest enrollment increase came from “community colleges with a high vocational program focus,” according to the National Student Clearinghouse Research Center. Demand for more focused, skills-based, career-oriented programs have long been a rallying point among students and higher ed reform advocates. Campus ($29 million Series B) is reinventing the community college experience by combining quality live, virtual instruction with skills-focused training programs.

Among four-year colleges, Arizona State University and Northeastern have built a strong reputation for workforce-integrated learning through strong employer and industry partnerships. They have been more of the exception; will others follow?

Elsewhere, companies have taken up the task of training and development talent earlier in the pipeline. My colleague Esteban Sosnik coined the term “verticalized edtech” to describe the emergence of companies solving labor market problems specific to an industry vertical, from training to placement and upskilling and HR support. RockED ($10 million Series A) is doing this for the automotive industry; Stepful ($7.5 million Seed) is training the healthcare workforce (another industry beleaguered by staffing shortages).

Just as schools and classrooms are changing, so too must workplaces retool their systems and operations to better attract, retain and support their people. For now, most AI applications have been focused on improving productivity and boosting efficiency. The bigger potential is in how it fundamentally transforms how we develop skills, access opportunities, and build stronger relationships — with ourselves and our communities.

Read the Latest

News and Insights