With Mega-deals on Hold, US Edtech Funding Slips to $2.2B in 1H 2023

The roaring twenties and the big, loud deals that opened this decade have come to a halt.

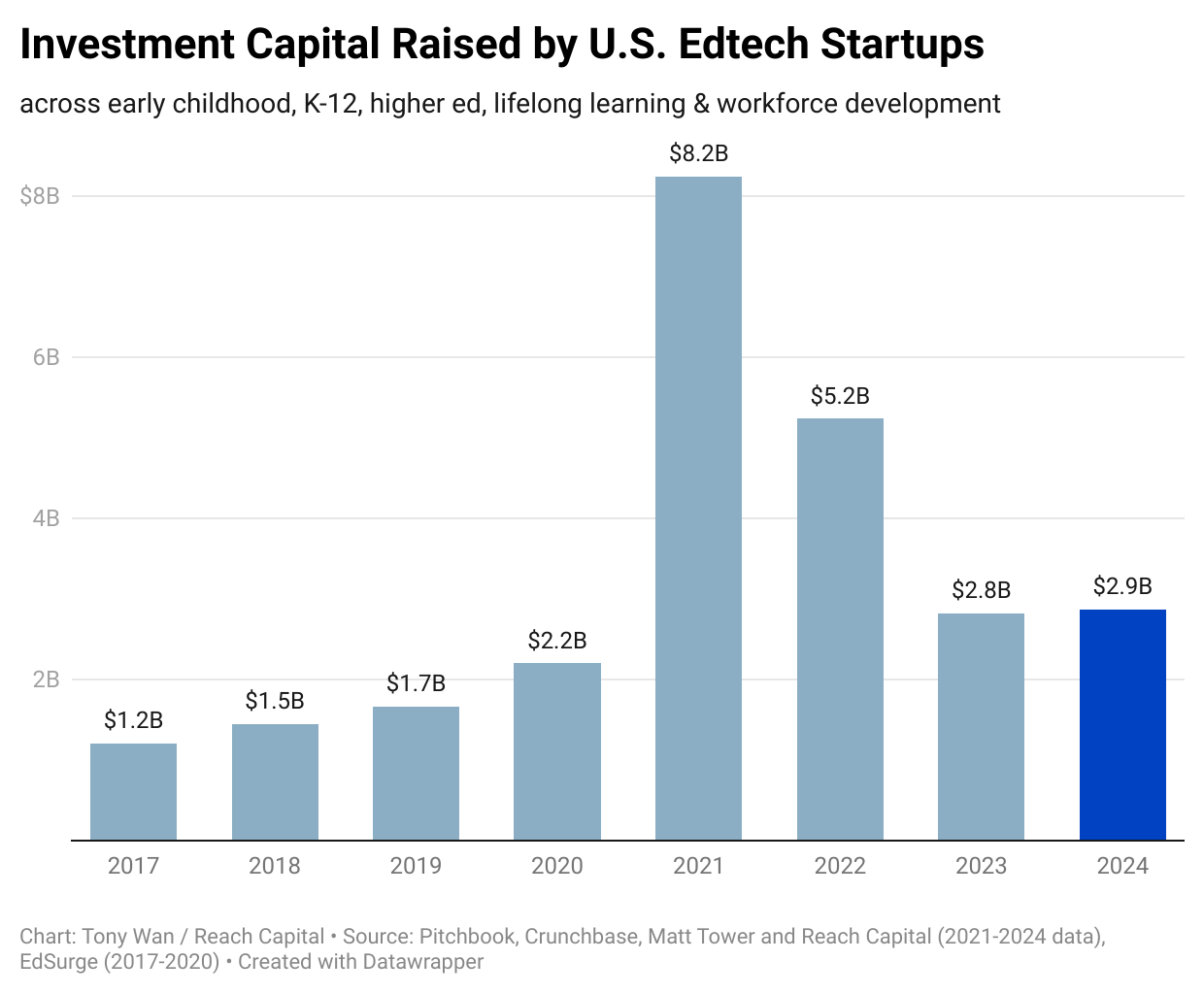

In the first half of 2023, private U.S. edtech companies raised $2.2 billion, according to our analysis of data from Pitchbook, Crunchbase and internal sources. That’s roughly two-thirds the amount raised during the first half of 2022 ($3.6 billion) and 2021 ($3.2 billion).

At this rate, the year-end tally for 2023 will surpass pre-pandemic levels, but fall short of the record $8.2 billion raised in 2021.

A sizable chunk of the $2.2 billion came from two publishers: Cengage’s $500-million growth round and Amplify’s $350-million Series C. These were two outsized, outlier deals for the edtech industry, which otherwise has seen a drop in invested capital amid a chill in the funding macroenvironment. One can argue these two publishers already had their belt-tightening moments prior to the current downturn.

For some context, total venture funding for all U.S. companies dropped 46 percent, from $158.8 billion in the first half of 2022 to $85.6 billion during the same period in 2023, according to Pitchbook. Global VC funding fell 53 percent year-over-year in Q1 2023.

Rising interest rates, the chilling of the IPO market and slashes in valuations have curbed the frothy investing enthusiasm that defined the pandemic heydays. With less capital sloshing about, the stress is on profitability and operational efficiency. It’s been painful for those that raised at the peak but are now struggling to grow into their valuations.

The edtech industry has bet heavily on the durability of digital experiences. Online education and remote work remain convenient, viable options, but Zoom school and Zoom meetings cannot fully replicate the benefits of being together in-person. Research continues to mount about the deleterious impact of fully-remote environments on educational achievement, mental wellbeing and work productivity. Our survey of our portfolio found that companies with onsite employees saw 3.5X higher revenue growth than those that were solely remote.

The pendulum is swinging back towards tools that effectively enable and enhance human connections. Human capital constraints (shortages of teachers, clinicians and other staff) are leading schools toward tech-enabled services connecting them to outside help for academics (tutoring and remediation), student support (mental health) and operations (transportation, substitute teachers and meals). In the workforce, training and keeping talent remains a priority as the labor market remains tight. “Even in a market downturn, those 20-25% who are high performers are always going to have options,” one HR leader recently told us. “Even if a company is doing layoffs and cutting budgets, they will still find ways to engage and retain that group.”

The renewed attention on human connection comes at a time when artificial intelligence is now on par with, and in many cases surpasses, human capabilities. AI tutors and assistants are proliferating in classrooms, homes and at work. The noise has been a wake-up call to incumbent companies and a catalyst for new upstarts looking to disrupt them. “What’s your AI strategy?” has been asked in likely every board meeting and earnings call.

Deal Trends

Mega-rounds on pause

The main driver for the funding dip is the near disappearance of the mega rounds.

Just two U.S. edtech deals surpassed $100 million in the first half of 2023; both happen to be publishers re-emerging from storied pasts. Textbook publisher Cengage received a $500-million injection from private equity firm Apollo Global to pay back a chunk of its debt from its bankruptcy nearly a decade ago. Amplify raised $350 million in a Series C from Cox Enterprises as it amasses a growing portfolio of K-12 digital curriculum and assessment tools that now reach nearly one-third of U.S. K-8 students.

Previous years saw 12 edtech mega-rounds in 2022, and 21 in 2021. Many of these deals were led by deep-pocketed investors — Coatue, Softbank, Tiger Global and others — that have since pumped the brakes. Some have lowered their fundraising targets for their new war chests. With the Tigers and investors of similar stripes retreating, so have the mega-rounds and minting of new unicorns.

Still, there’s a healthy stable of unicorns lying in wait for the IPO window to reopen: Guild Education, Outschool, BetterUp, Course Hero, Lovevery, and Handshake, among others. The edtech industry last enjoyed its breakout in 2021 when Coursera, Duolingo, Powerschool and Instructure went public. Will 2024 be the year?

Early-stage deals hold steady, though at lower valuations

While the growth rounds have become scarce, early-stage opportunities remain abundant (as our pipeline attests to). Funding should hold steady as well; we recently closed a new fund as did New Markets, another longtime edtech-focused investment firm.

The biggest seed deal went to Proof of Learn, which raised $19 million in a seed round led by NEA for its Web3 education and talent development marketplace. (Remember Web3?) Excluding this outsized, outlier seed deal, the average seed round was $2.7 million, which is close to previous years. Check sizes for Seed and Series A have been holding steady compared to 2022, though the average valuation has ticked down.

As in previous years, workforce development tends to command larger check sizes and valuations. The next biggest seed deal, at $7.5 million, went to healthcare workforce training startup Stepful, which we led. Higher-ed startups also scored sizable Series A rounds: UWill raised $30 million for its mental health and wellness platform for colleges and students; Campus raised $29 million to reinvent the community college experience.

The AI premium

Bucking the overall funding downturns are, of course, the new generation of AI tools, led by OpenAI’s ChatGPT and closely followed by competitors across the spectrum, from Google to upstarts. Here there have been plenty of megarounds and mega-acquisitions (like Databricks’ $1.3 billion acquisition of MosaicML). Similar to Web3 not too long ago, AI is commanding a valuation and investment premium.

Replit raised the second largest round so far in 2023 for a U.S. edtech startup with its $97 million Series B extension. Beginning as a browser-based coding platform, the company has been swiftly shipping AI features (like the coding assistant Ghostwriter) to be the next go-to-shop where people learn and build with code. In March it announced a partnership with Google that will further power its AI software development tools.

Beyond the U.S. AI edtech companies are securing big checks. At the seed stage, Israeli language-learning platform Loora recently raised $9.25 million; so did Kinnu, a U.K.-based mobile-learning app, which just notched $6.5 million (following its $2.4 million pre-seed). In Sweden, Sana Labs, an AI-powered learning platform for corporate learning, raised an additional $28 million for its Series B, pushing the round total to $62 million.

AI education companies with defensible businesses and product-market fit will continue to attract attention, even from generalist investors that have otherwise stayed on the sidelines in education deals this year. Firms like a16z are putting out AI education investment theses to signal their interest.

Show me results

AI or not, any technology’s market longevity hinges on its ability to solve real, critical problems. Just as the market is scrutinizing business operational efficiency, schools and workplaces are now more discerning about impact and efficacy.

“A lot of investment has been made in recent years around technology, and right now there’s a lot of focus on simplifying the tech stack and maximizing ROI,” David Landman, Global Head of Talent Development at Goldman Sachs, told us. “There’s a focus now on reviewing what HR teams have brought onboard and evaluating the success of programs and technology.”

There is a trend toward consolidation in schools as well. The latest report from LearnPlatform found that in any given district, students and educators accessed nearly 2,600 different educational websites and tools over a year. Some districts are trending toward usage-based pricing for software contracts (versus fixed seat licenses), perhaps in response to the deluge of tools that many schools paid for but rarely used.

“Teachers and students are engaging with fewer edtech products to learn, but the diversity of options is forcing organizations to manage even more digital tools than last year,” LearnPlatform’s co-founder Karl Rectanus noted. “Evidence-based edtech and platforms will likely drive purchasing, decision-making, and effective teaching and learning.”

Read the Latest

News and Insights