What Are the Pros and Cons of Fundraising from Venture Capital Versus Private Equity?

Dear Guido,

My company is currently fundraising and we have received interest from venture capital and private equity firms. What are the pros and cons of each? How do I weigh which source of capital is right for me?

— Frantically Fundraising

Hi Frantically Fundraising,

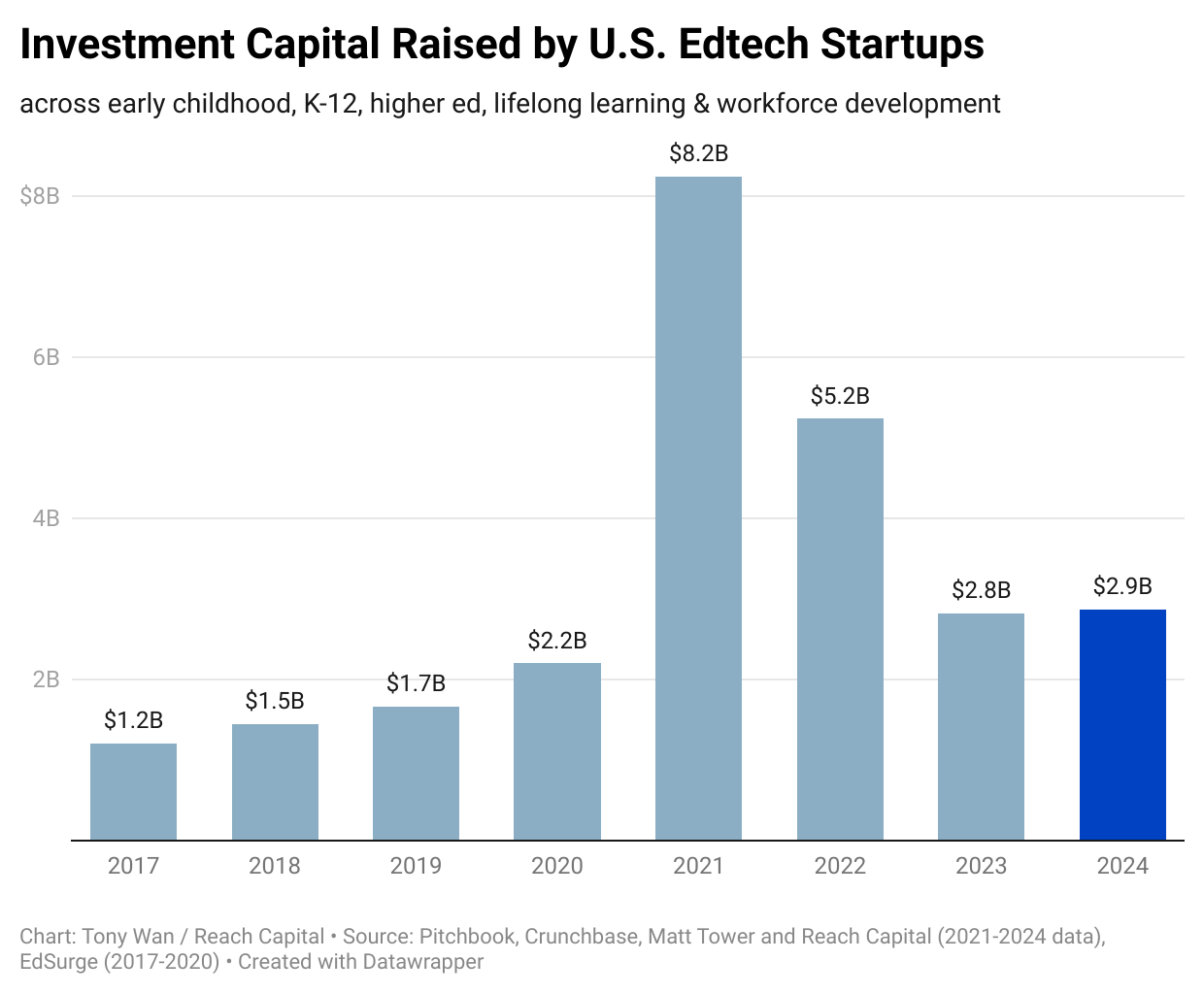

First, congratulations! Timing is everything, and this is an incredible environment for fundraising. Back in the early years of the last decade, there were only a handful of edtech-focused funds interested in the education market. Now, we’re seeing brand name players like General Atlantic and Tiger Global jump on the edtech bandwagon.

So your situation is not uncommon. At Nearpod, we raised a mix of angel and venture capital for our seed and Series A rounds. When we went out to fundraise again in 2016, we ultimately chose to join forces with private equity firm Insight Partners. Insight led our $21 million Series B round, and it was joined by returning investors Reach Capital and GSV Ventures.

We recently sold Nearpod to Renaissance Learning, which is also backed by a large private equity firm. When reflecting on our journey, we were fortunate to have great partners from both VC and PE backgrounds to help us grow and land a great outcome. But there are important distinctions between the two that can shape the trajectory of your journey.

The Pros of Private Equity

The most obvious upside to partnering with a PE firm is money. Private equity firms usually have much deeper pockets than venture capital firms. And especially in edtech, where by the time you’re raising a Series B or C, few of the edtech-specific folks have enough powder to write a $50 million check.

PEs also provide additional access to funds for operational and strategic activities. These firms have well-established connections with banking partners, which can provide additional funding (typically in the form of venture debt) in case you are pursuing acquisitions. While we had looked at several targets before, we acquired just one company during my time at Nearpod — Flocabulary (an educational hip-hop company). As soon as we decided to pursue this deal, we put a plan together, discussed it with our board, and Insight quickly got the ball rolling to get us a few debt term sheets in a matter of days. It was amazing.

Another PE value-add are the large teams of in-house analysts available to help for these sorts of opportunities. They can help by scanning the market, calling up the right people, helping with diligence, and working with your CFO to get the numbers right. You’re still in charge of the acquisition process, but this support effectively expands your internal capacity by several people who work closely with you just to get the deal done.

We looked at several other potential acquisitions and ultimately decided not to pursue them. But if we had chosen to, the funding and the support would have been available thanks to our close relationship with our PE partner.

Lastly, private equity firms are also generally more open to doing deals where they buy secondary shares. This is important to consider if you or your team have been working very hard for years, and you want to have an opportunity to sell some shares while still staying involved with your startup.

Things to Know About the Private Equity ‘Playbook’

Private equity capital comes with certain constraints. Most firms operate formulaically and go by a playbook to ensure that you get the capital to help you scale what you’re already doing. This can be a little limiting but it’s not entirely a straitjacket; you can grow your sales team if you’re pursuing international expansion, for example. But, in my experience, they will be less likely to give you a blank check if you want to invest a lot in R&D to explore new opportunities beyond your current core offering.

Most PE firms also have a pretty strict timetable and threshold for how long they’ll hold a company before wanting to sell. By the time a company meets their IRR benchmarks and enters “exit territory,” they’ll usually be inclined to sell, even if there are interesting growth opportunities in the future. PEs are generally satisfied with a lower return on their investments than what VCs would like (say, 3X versus 10X).

The driver for Nearpod’s exit was a combination of some stellar numbers, accelerated by a growth in adoption during the pandemic, a recent leadership transition and a considerable amount of interest among potential buyers. At the time, Nearpod had been in Insight’s portfolio for over four years, and we had achieved a certain revenue size and growth level that made us ripe for a big sale.

The VC Advantage: More Flexibility

If your startup is at a stage where you’re still exploring new ideas and markets, or you are considering making changes to the core business to pursue new opportunities, venture capital may be the better partner for you. From my experience, VCs are more ambitious dreamers, and as long as they’re onboard with your vision, they’ll support investing in research and development and experimentation.

This makes it easier to pivot your business or product as you feel is necessary. If a VC sees an opportunity to get a 20X return on their investment, versus 10X, they’ll want to do it. As long as you’re growing and hitting your goals, I’ve found VCs to be less strict on the timing of an exit.

VCs also tend to be less likely to be micro-managers. Yes, there are the quarterly board meetings and reporting requirements. And sure, VCs will give you plenty of feedback on strategy and on the most relevant corporate matters. But for the most part, they are pretty hands off when it comes to execution. PEs, which will usually take a bigger controlling stake in your company, are not. They wield veto power over decisions they don’t like.

If you choose to pursue VCs for later-stage rounds, one thing that is important to get right is making sure that they get along with the existing board members. I’ve seen VC-backed companies where the founders didn’t really have control of the board, and the board dynamics became quite dysfunctional when things weren’t going extremely well.

This usually isn’t an issue with PE firms that often take multiple board seats, in which case you’re dealing with just one set of decision makers. That was the situation with Nearpod, and for the most part we were able to build a very functional board and maintained good working relationships with all the directors.

Whether you pursue venture capital or private equity, I cannot underscore enough how much you need to do due diligence on the people you will work with. My friend Jennifer Carolan (who invested in us many times and sat on our board) has written a great post outlining the five questions you should ask every investor. Check it out!

Read the Latest

News and Insights